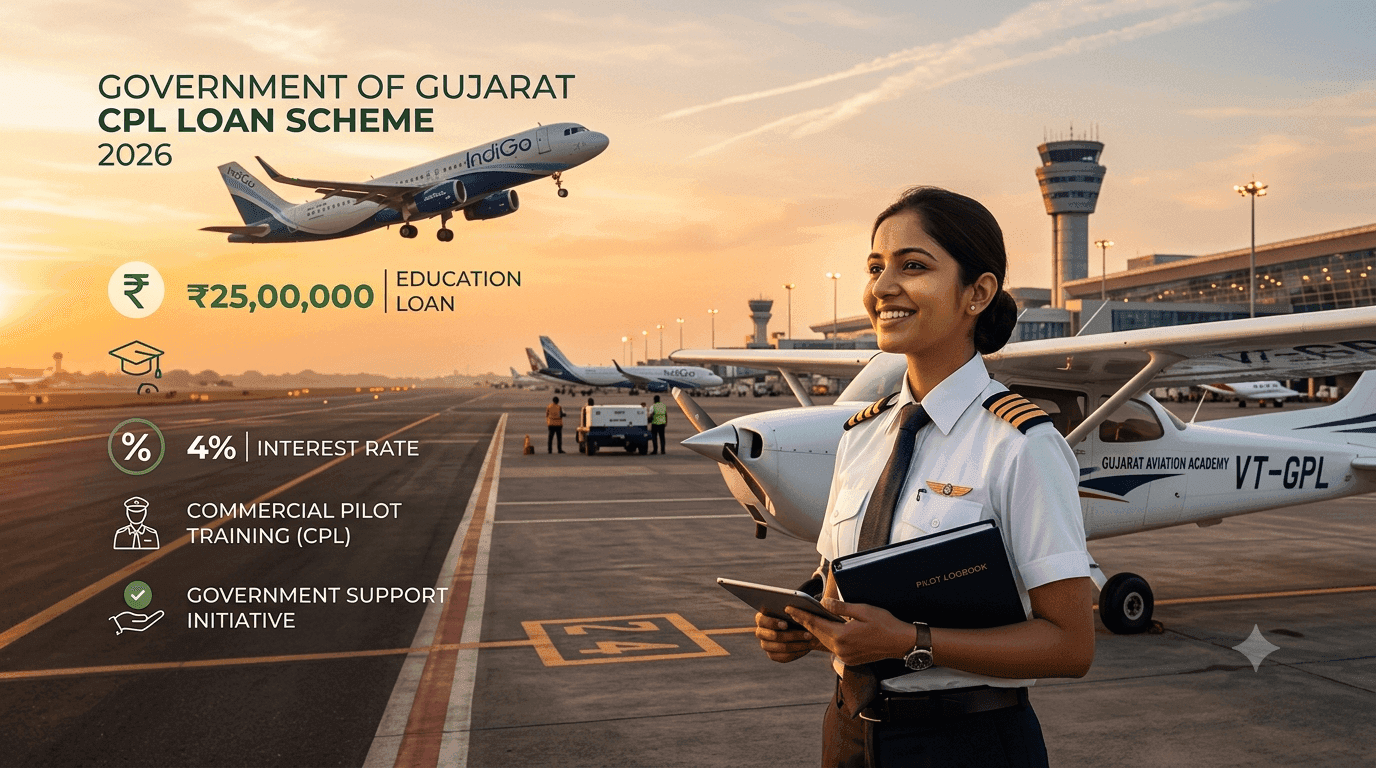

1. What Is the Gujarat Government Pilot Training Loan Scheme?

India's aviation sector is growing at a pace that few other industries can match. Yet beneath that growth lies a real and pressing problem: there simply are not enough qualified commercial pilots to keep up with demand. The Gujarat state government recognised this gap and responded with a dedicated loan scheme designed to help aspiring pilots from the state fund their flight training.

The scheme was built around one clear objective — to remove the single biggest obstacle most candidates face. Obtaining a Commercial Pilot Licence (CPL) is expensive. Costs can run into tens of lakhs of rupees, placing the dream of a flying career well beyond the reach of many families. By facilitating access to credit for pilot training, Gujarat aims to develop home-grown aviation professionals and reduce reliance on pilots trained elsewhere in India or abroad.

The scheme is administered through the Gujarat government's nodal financial and aviation development authorities, working in coordination with empanelled banks and lending institutions. These bodies carry out a defined set of responsibilities: evaluating and approving eligible applicants, disbursing funds directly to approved flight training organisations, and monitoring repayment schedules to ensure accountability. Since implementation details can change between policy cycles, applicants are advised to verify the current administering authority directly through the Gujarat government portal.

This initiative does not exist in isolation. India's UDAN regional connectivity scheme has significantly expanded the number of operational airports and active flight routes across the country. That expansion translates directly into greater demand for trained pilots — demand that the current supply of aviation professionals cannot adequately meet.

Gujarat's loan scheme fits squarely into this national picture. It creates a state-level pipeline of aviation talent that feeds into a rapidly growing industry. For candidates from middle-income families, the scheme carries considerable weight. It opens doors to a career that was previously accessible only to those with substantial personal wealth. In doing so, it also contributes to India's broader capacity to staff its expanding fleet of regional and commercial aircraft.

Need personalised guidance before you apply?

Book a free consultation with our aviation experts for personalized guidance.

👉 Get Free Career Consultation

📖 Plan your full journey from student pilot to commercial aviation career. Career Roadmap for the Aspiring Commercial Pilot

2. Eligibility Criteria: Who Can Apply for This Loan Scheme?

There isn't one single scheme — there are three, run in parallel

Gujarat doesn't offer this as a single, unified loan. It runs as three separate, category-based schemes, each administered by a different state body, sharing the same ₹25 lakh cap and 4% interest rate:

- Scheduled Caste (SC) applicants — administered by the Director, Scheduled Caste Welfare, under scheme BCK-14.

- SEBC (Socially and Educationally Backward Classes) applicants — administered by the Director, Developing Castes Welfare.

- Unreserved (General) category applicants — administered by GUEEDC, the Gujarat Unreserved Educational & Economic Development Corporation.

Which one an applicant uses depends entirely on category. The requirements below apply across all three unless noted.

Domicile and Academic Requirements

- Domicile: Must be a permanent resident of Gujarat, with a valid domicile certificate at the time of application — this applies across all three tracks.

- Academic qualification: This is where the tracks differ. The SC scheme's own guidelines set the bar at SSC (10th standard) pass or above. The SEBC and Unreserved/GUEEDC tracks generally require HSC (12th standard) pass — confirm the current SEBC wording with the Developing Castes Welfare office, since we found this stated clearly for SC and GUEEDC but not spelled out as explicitly on the SEBC page itself.

- A note on Physics and Maths: None of the three schemes state a PCM (Physics-Chemistry-Maths) requirement as a loan condition. That comes from DGCA and the training institute as part of CPL admission itself — it's implicit in "having secured admission," not a separate eligibility rule for the loan. Worth keeping these distinct: a student without PCM isn't disqualified from the loan, only from CPL admission until that's cleared.

Age

None of the three schemes state an age limit in their published guidelines. The practical floor comes from DGCA's own training requirements (17–18, depending on licence stage), not from the loan scheme — so there's no basis for telling an applicant over 30 they're ineligible on age alone.

Income — There Is No Ceiling

Worth stating plainly, since it cuts against what most people assume about a welfare loan: all three tracks explicitly state there is no family income limit. Applicants across every economic bracket within their category qualify. An income certificate is still part of the document checklist, but for records rather than as a qualifying threshold.

Medical Fitness Requirements

Separately from the loan scheme's own conditions, CPL training itself requires a DGCA-issued medical certificate:

- A Class 2 Medical Certificate to begin training.

- A Class 1 Medical Certificate before the CPL skill test stage.

Both are issued by DGCA-authorised aviation medical examiners. This is a training-entry requirement rather than a loan-scheme-specific rule, but every applicant will need it regardless of which of the three tracks they apply under.

📖 Understand which exam topics repeat most before you begin pilot training. DGCA Previous Year Question Analysis 2026: Patterns

3. Loan Amount, Coverage, and Repayment Terms

Maximum Loan Amount

Each of the three tracks — SC, SEBC, and Unreserved/GUEEDC — caps the loan at ₹25,00,000. This is a fixed ceiling set in the scheme guidelines, not a variable figure that depends on the lending institution or the applicant's profile.

What the Loan Covers

The loan is disbursed against the fee receipt from the training institute the applicant has been admitted to, rather than against a scheme-defined breakdown of expense categories. In practice, the ₹25 lakh ceiling needs to cover whatever the admitted flying school's total course fee comes to. Applicants training at institutes whose full CPL cost exceeds this ceiling will need to arrange the difference separately.

Interest Rate and Repayment Structure

The interest rate across all three tracks is 4% per annum, simple interest — well below the 9–12% typical of a standard bank education loan. We didn't find a gender-based rate concession specific to this scheme (unlike some other Gujarat education loans, which do offer one), so the 4% applies uniformly regardless of applicant gender.

Repayment follows a specific structure worth stating precisely rather than approximating:

- A moratorium of one year from the date of disbursement before any repayment begins.

- Principal is then repaid over up to 10 years, in equal monthly instalments (or quarterly, if requested in advance).

- Interest becomes payable only after the principal is fully cleared, repaid on the same instalment basis — bringing the effective total repayment window to as much as 12 years.

- A 2.5% penal interest applies on late or missed instalments, and continued default escalates to recovery through Revenue Recovery procedures — a more serious enforcement mechanism than a typical bank loan default.

Security and Guarantor Requirements

The scheme guidelines don't specify a margin-money percentage the way a conventional bank loan might. Security is handled through collateral and guarantors instead. Commonly documented requirements — confirm the current version with the relevant office before advising applicants — include two guarantors with property documents, a surety bond, and, for the SC track specifically, a stamp-paper undertaking to work in India for at least five years after training. If the beneficiary settles abroad after training, the full loan and interest becomes repayable immediately.

Not sure which aviation path fits your profile? Book a free consultation with our aviation experts for personalized guidance. 👉 Get Free Career Consultation

4. Step-by-Step Application Process and Required Documents

Where and How to Submit Your Application

Most states that offer a government loan scheme for pilot training provide both online and offline application routes. The online portal is usually hosted on the official state finance or education department website. Applicants create an account, fill in their personal and academic details, and upload scanned copies of the required documents. Those applying offline must visit the designated district-level nodal office, collect the prescribed form, and submit a physical file with attested copies of all documents.

Always verify the portal URL directly from the official government website. Third-party links can be fraudulent, and accessing the wrong portal puts your personal information at risk.

Complete Document Checklist for Applicants

Gathering the correct paperwork before you begin is the single most effective way to avoid delays. Prepare the following:

- Domicile certificate issued by the competent authority of your home state.

- Income proof — a family income certificate or the latest Income Tax Return of the guardian or applicant.

- Confirmed admission letter from a flying school approved by the DGCA (Directorate General of Civil Aviation).

- Academic transcripts — Class 10 and Class 12 mark sheets, with Physics and Mathematics clearly mentioned.

- Medical fitness certificate — a Class 1 or Class 2 medical certificate issued by a DGCA-authorised aviation medical examiner.

- Passport-size photographs, Aadhaar card, and bank account details for disbursement.

One point deserves particular attention: an admission letter from a flying school not listed on the DGCA-approved roster is the most common reason applications are outright disqualified. Confirm the school's approval status on the DGCA official website before paying any fees.

Timeline: From Application to Loan Disbursement

Once a complete application is submitted, the process generally moves through three stages:

- Document verification (2–4 weeks): Nodal officers review the submitted documents for completeness and authenticity.

- Sanctioning authority approval (3–6 weeks): The file is forwarded to the sanctioning committee, which may request additional clarifications before a decision is made.

- Loan agreement and disbursement (1–2 weeks): Once approved, the applicant signs the loan agreement and funds are transferred directly to the flying school or the applicant's bank account.

The total end-to-end timeline is generally 6 to 12 weeks from the date a complete file is submitted. Incomplete documents, mismatched information, or a missing medical certificate are the most frequent causes of delays. Go through every item on the checklist carefully before you submit.

📖 Know exactly what subjects and sections the CPL licensing exam covers. DGCA CPL Exam Pattern & Syllabus 2026

5. How to Maximise Your Chances and Next Steps After Approval

Securing a government loan scheme requires more than simply submitting an application. Lenders assess your profile carefully, and a few deliberate steps can make a meaningful difference to the outcome.

Begin by ensuring your credit history is in order. Check your credit report well in advance and address any discrepancies or outstanding dues. A clean repayment record signals reliability to lenders and can strengthen your application considerably.

Prepare your documentation thoroughly before you apply. Incomplete paperwork is one of the most common reasons for delays or rejections. Gather your identity proof, address verification, income statements, and any business-related documents if applicable. Having everything organised from the outset demonstrates seriousness and saves time.

Choose the scheme that aligns most closely with your specific circumstances. Each government loan scheme carries its own eligibility criteria, interest structure, and end-use conditions. Applying for a scheme that genuinely fits your profile reduces the risk of rejection and ensures you benefit from the terms designed for your category.

Once your application is approved, the work does not stop there. Read the sanction letter carefully and understand every condition attached to the loan. Pay close attention to repayment schedules, moratorium periods if any, and penalties for late payment.

Use the funds strictly for the stated purpose. Diverting loan amounts can lead to complications during audits or follow-up assessments, particularly under government-backed schemes where end-use verification is standard practice.

Maintain a consistent repayment record from the very first instalment. This not only keeps you in good standing with the lender but also builds a stronger credit profile for any future borrowing needs. Timely repayment under a government scheme can open doors to higher loan limits or preferential terms down the line.

Ready to take the next step in your aviation journey?

Book a free consultation with our aviation experts for personalized guidance.

👉 Get Free Career Consultation